Introduction - The Importance of Share Capital in the Formation of a GmbH

Share capital is a central element when it comes to founding a Gesellschaft mit beschränkter Haftung (GmbH). It represents the financial foundation of the company and serves as a guarantee for creditors and business partners. In the process of establishing a GmbH, share capital acts as a clear indicator of the company's seriousness and reliability.

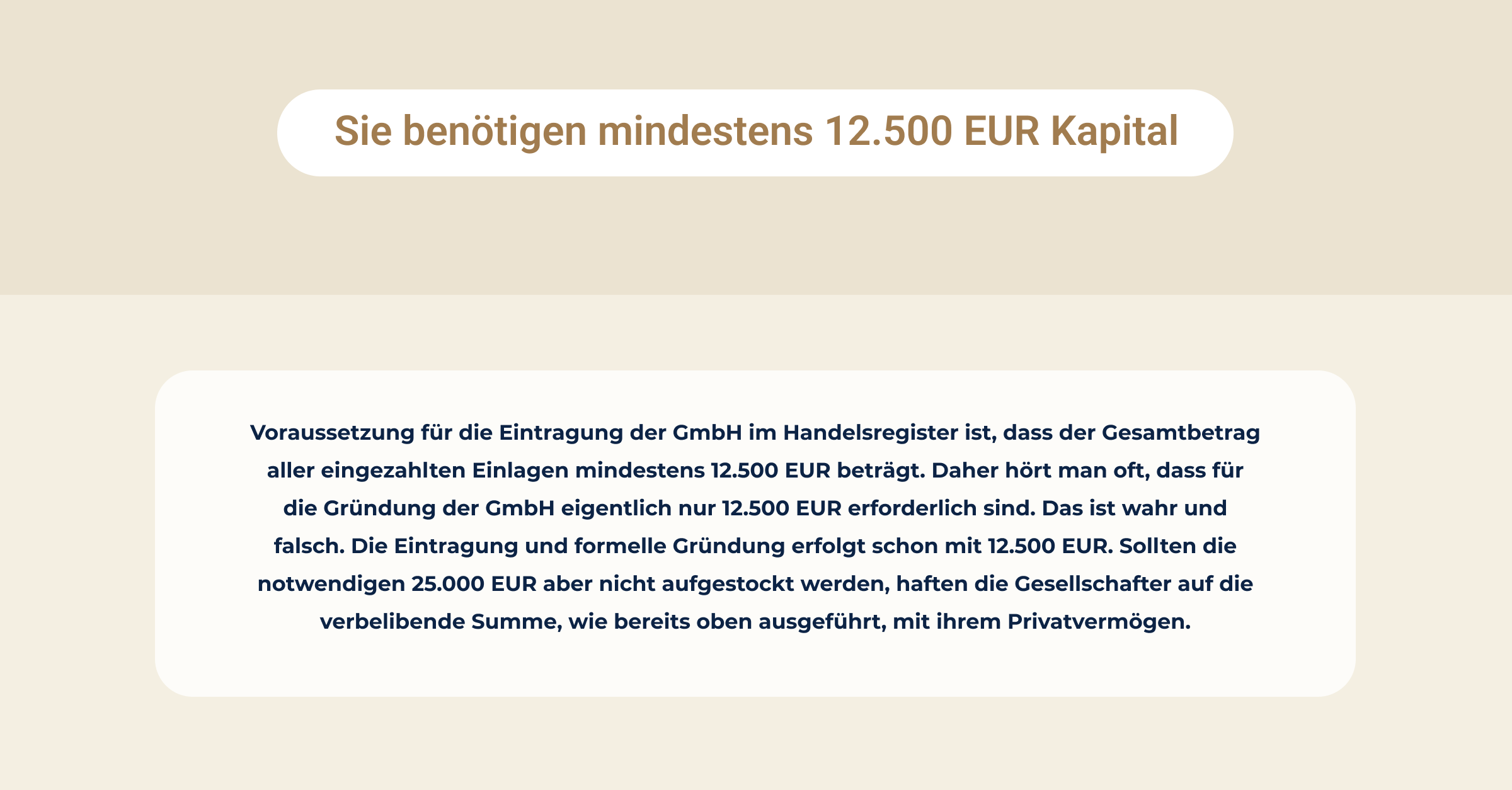

In Germany, the minimum share capital for a GmbH is legally defined. According to § 5 of the GmbH Act (GmbHG), it amounts to €25,000. This share capital can be contributed in the form of cash or non-cash assets. At least half of this amount, or €12,500, must be deposited before the GmbH can be registered.

The share capital directly impacts the liability in a GmbH. It serves as a security mechanism that allows shareholders to remain protected with their personal assets. In the event of insolvency, the GmbH is liable only up to its share capital, which minimizes the personal risk for shareholders.

It’s not just the amount of share capital that matters, but also how it is utilized. The capital must be exclusively used for business purposes. Any misuse of the share capital can lead to legal consequences and compromise the company's limited liability. The use of share capital is strictly regulated by laws and provisions to prevent abuse and to ensure the protection of creditors.

What is meant by share capital when founding a GmbH?

The share capital is the financial base that must be deposited when founding a GmbH. It serves as the foundation for business activities and provides a certain level of security for creditors and business partners. The share capital is not only a legal requirement but also an indicator of the GmbH's financial stability.

According to § 5 GmbHG, the minimum share capital for a GmbH in Germany is set at 25,000 euros. At least 12,500 euros must be paid as a cash contribution at the time of the GmbH's registration, with the remaining amount to follow later. The share capital can be contributed in the form of cash or non-cash assets, such as vehicles, machinery, or real estate.

The share capital has a dual function: it ensures that the GmbH has a financial basis to commence its business activities, and it limits the shareholders' liability to the amount of the share capital. Shareholders are not liable with their private assets as long as they comply with legal regulations.

A GmbH must use the share capital to finance its operations and cover ongoing expenses. The law stipulates that the share capital cannot be used for private purposes. Violations of these regulations can lead to legal consequences, including personal liability for the shareholders.

In some cases, courts have ruled that shareholders lose the limitation of liability if the share capital is misused.

To establish a GmbH, you need more than just the share capital, and for many steps, collaboration with a notary is not only recommended but absolutely necessary. This includes, for example, the registration in the commercial register. If you want to save time and handle the appointments online, beglaubigt.de helps you find the right notary.

Send us a request to establish a GmbH, and we will arrange an online appointment with a suitable notary near you.

How much must be paid in when founding a GmbH?

When founding a GmbH, depositing the share capital is an essential step. The minimum share capital required for a GmbH in Germany, according to § 5 GmbHG, is 25,000 euros. However, it is not necessary to pay this amount in full immediately. At least half of the share capital, i.e., 12,500 euros, must be paid in at the time of the GmbH's registration.

The remaining capital can be contributed later. This regulation allows for a certain degree of flexibility during the founding process and ensures that the GmbH has a solid financial foundation before starting its business operations. However, there are strict deadlines and requirements that must be followed.

The deposit of the share capital can be made in different forms. The most common is a cash contribution, where the corresponding amount is deposited into the GmbH's business account. Alternatively, non-cash assets such as real estate, vehicles, or machinery can be contributed as share capital. In this case, these non-cash assets must be properly valued and documented to meet legal requirements.

It is important to note that the contributions must be available at the time of the company's formation. Attempts to fictitiously contribute the share capital or to not use it for business purposes can lead to legal consequences and endanger the limitation of liability. In the past, court decisions have resulted in personal liability for shareholders when violations of these regulations occurred.

To successfully and legally establish a GmbH, many other steps must also be taken into account. You can find more information about this here: Steps to Founding a GmbH

Can you found a GmbH with 12,500 euros?

Yes, a GmbH can be founded with a cash contribution of 12,500 euros, provided certain conditions are met. According to § 5 GmbHG, the minimum share capital for a GmbH is 25,000 euros. However, it is sufficient if at least half of the minimum share capital, i.e., 12,500 euros, is paid in at the time of registration.

Now new: Beglaubigt.de accompanies your entire founding process: Start a GmbH

This amount is often referred to as the "minimum share contribution" and serves as the basis for starting business operations. It is essential that the capital is actually available and deposited into a business account of the GmbH. The deposit is verified by a bank confirmation, which must be submitted at the time of registration.

The remaining amount required to reach the full share capital can be contributed later. However, it is important to note that the deposit of the remaining capital is subject to certain deadlines and conditions. Shareholders are obligated to comply with these requirements to avoid jeopardizing their limited liability.

It is also crucial that the deposited capital is used exclusively for business purposes. Misuse or inappropriate use of the share capital can lead to legal consequences and affect the limited liability of the GmbH. Court rulings in the past have shown that violations of these rules can result in personal liability for shareholders.

In summary, the option to found a GmbH with a cash contribution of 12,500 euros offers some flexibility. However, it also presents challenges in terms of complying with legal requirements and the correct use of capital.

If you want to save time when founding your GmbH, many steps can also be completed online. If you have any questions about our service and how we can assist you in the founding process, feel free to contact us. If you'd like to learn more about online company formation, the following article might be of interest: The Digital Notary for Germany – Online Formation of a GmbH or UG.

What happens with the 25,000 euros in a GmbH?

The share capital of 25,000 euros is a legal requirement to establish a GmbH in Germany. It represents the financial foundation of the company and serves as a safety net for creditors and business partners. Once the cash or non-cash contributions are made, they must be deposited into a business account of the GmbH and used exclusively for business purposes.

It is crucial that the share capital is not used for personal expenses or non-business-related purposes. The GmbHG (German Limited Liability Companies Act) imposes strict penalties and liability risks in such cases. Violations of these regulations can lead to shareholders losing their limited liability protection and becoming personally liable.

The share capital is often used for the following purposes:

- Business setup: Investments in infrastructure, equipment, and personnel.

- Operations: Covering ongoing operating costs such as rent, salaries, and taxes.

- Reserves: Creating a financial buffer for unforeseen expenses or economic challenges.

It is essential for the GmbH to maintain clear accounting records to document the use of the share capital and comply with legal requirements. Regular audits by external auditors can help ensure that the GmbH operates correctly and avoids violations.

Court rulings in the past have shown that improper use of share capital can have legal consequences. In some cases, shareholders were held liable for financial damages because they did not use the share capital properly or misused it. Therefore, when founding a GmbH, it is essential to use the share capital responsibly and in accordance with legal regulations.

In addition to the required share capital, there are other costs associated with founding a GmbH. Here is an overview of the expected costs: Costs of founding a GmbH.

Why must start-up capital be contributed when founding a GmbH?

Contributing start-up capital when founding a GmbH is necessary for several reasons. The first reason is legal: § 5 of the German Limited Liability Companies Act (GmbHG) requires a minimum share capital of 25,000 euros for a GmbH. Without this capital, a GmbH cannot be officially established or registered in the commercial register. The provision of start-up capital ensures the company's financial foundation and demonstrates that the founders have sufficient resources to begin business operations.

Another reason is to protect creditors. The share capital serves as security for creditors who do business with the GmbH. It shows that the company has funds to meet its obligations and settle potential debts. Without this start-up capital, creditors would be exposed to greater risks if the GmbH became insolvent.

Start-up capital also limits shareholder liability. In a GmbH, liability is limited to the amount of share capital, meaning that shareholders are not personally liable in the event of insolvency. This limitation makes the GmbH an attractive corporate form for entrepreneurs who wish to minimize their personal risk.

The provision of start-up capital ensures that the GmbH can begin and sustain its business activities. Without a minimum level of capital, investments in infrastructure or staff could not be made, which could jeopardize the business.

Finally, the start-up capital contributes to the credibility of the GmbH. It shows business partners and customers that the company is on a solid financial footing. This is particularly important in the early stages of business when stakeholder trust is crucial.

Complying with legal requirements and responsibly managing the start-up capital is not only mandated by law but also essential to the success of the GmbH.

Can the share capital of a GmbH be used for personal purposes?

The share capital of a GmbH cannot be used for personal purposes. It is intended solely for the business activities of the company. The rules and laws governing share capital are strict to ensure that the capital is used to secure the financial foundation of the GmbH and protect creditors. If the share capital is used for private purposes, it can lead to legal consequences and endanger the limited liability of the GmbH.

According to § 30 GmbHG, it is prohibited for a GmbH to use its share capital to cover personal expenses of shareholders or managing directors.

Violations of this provision can be considered as illegal withdrawals, which can result in criminal consequences. In such cases, shareholders may lose their limited liability and be personally liable for losses or debts of the GmbH.

Examples of misuse of share capital include:

- Private purchases: When shareholders or managing directors use the GmbH’s funds for personal expenses such as cars, vacations, or other non-business-related purposes.

- Illegal withdrawals: Taking money from the share capital without proper accounting or justification.

- Improper use: Using the share capital for investments or projects that are not in line with the GmbH's business purpose.

To ensure that the share capital is used correctly, the GmbH must maintain clear accounting records and undergo regular audits by external auditors. This ensures transparency and prevents misuse. Additionally, any withdrawals or expenses from the share capital should be well-documented and legally reviewed.

In summary, using the share capital for personal purposes is a serious violation of legal requirements and can have far-reaching consequences. Companies should therefore ensure that the share capital is used correctly and in compliance with legal regulations to avoid legal risks and maintain the GmbH’s credibility.

We want to help make your GmbH formation as quick and easy as possible. That’s why we work with notaries across Germany to provide you with a professional from your region.

How does share capital affect liability in a GmbH?

The share capital of a GmbH directly impacts the liability of its shareholders. One of the main advantages of a limited liability company (GmbH) is the limited liability that protects the personal assets of the shareholders. As long as the GmbH complies with legal requirements, shareholder liability is limited to the amount of the share capital.

According to § 13 GmbHG, the GmbH is a separate legal entity. This means that the company’s debts and obligations do not extend to the shareholders. In the event of insolvency, the GmbH is liable only with its share capital, shielding shareholders from being personally held accountable for the company's debts.

However, there are exceptions where the limitation of liability can be lifted:

- Negligent or intentional actions: Shareholders or managing directors may be personally liable if they act negligently or intentionally, such as through misuse of the share capital or gross violations of duty.

- Commingling of assets: If the share capital is used for personal purposes or mixed with private assets, the limitation of liability may be voided, leading to what is known as "piercing the corporate veil" (Durchgriffshaftung).

- Liability to third parties: In certain cases, such as fraud or misrepresentation, shareholders can be personally liable to third parties.

Therefore, it is crucial that the GmbH maintains its financial integrity and uses the share capital exclusively for business purposes. Regular audits and clear accounting practices ensure proper use of the share capital.

To maintain the limitation of liability, shareholders and managing directors must strictly adhere to legal obligations and handle the share capital with care. Violations can result in legal consequences and damage the GmbH’s credibility.

Summary

Share capital is a fundamental component of forming a GmbH. It forms the financial foundation of the company and sets the liability limits of the shareholders. German GmbH law requires a minimum share capital of 25,000 euros, with at least half of this amount to be paid at the time of the company’s formation. This requirement ensures financial stability and guarantees that the GmbH can meet its obligations.

Share capital also influences the limitation of liability in a GmbH. As long as the company fulfills its legal obligations and uses the share capital properly, the shareholders are not personally liable for the company’s debts. Adhering to rules, particularly regarding the use of share capital for business purposes, is essential to avoid the risk of personal liability.

Improper use or commingling of share capital with personal funds can have serious consequences, including the removal of limited liability protection. Court rulings have shown that shareholders who violate legal provisions may be held personally liable for company debts.

Additionally, share capital plays a key role in building trust with creditors and business partners. A solid financial foundation enhances the credibility of the GmbH and facilitates access to resources and business opportunities. Thus, properly contributing and responsibly managing share capital is critical to the successful formation and operation of a GmbH.