What is a loan agreement, explained simply

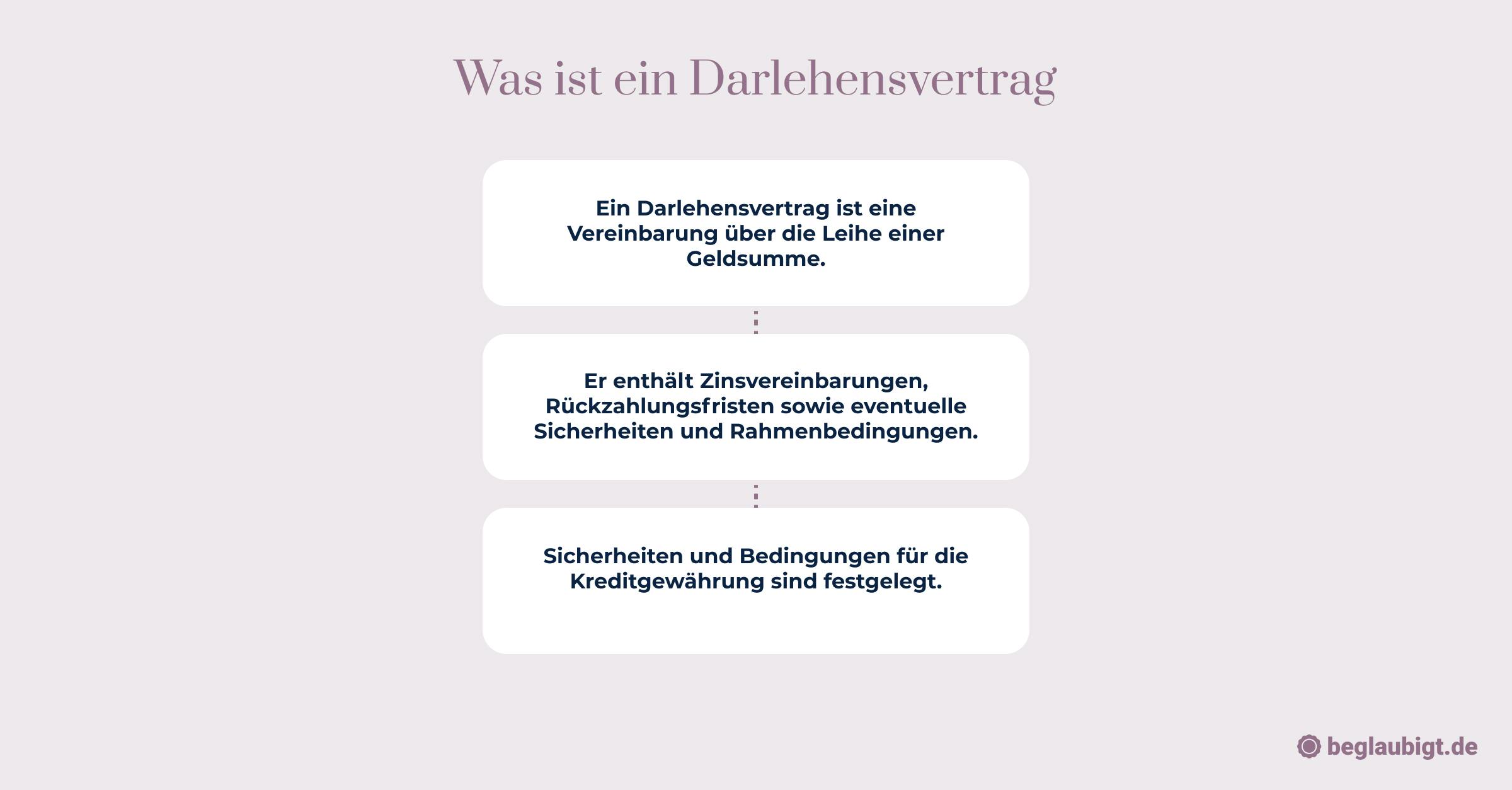

A loan agreement is essentially a contractual agreement between two parties in which one party (the lender or creditor) provides the other party (the borrower) with a certain amount of money for an agreed period of time.

In return, the borrower undertakes to repay this amount within the specified period plus agreed interest.

The basic concept is therefore the exchange of present money for the promise of future payments.

Unlike other financial instruments such as stocks or bonds, where the value often depends on market movements or the performance of the issuing company, a loan agreement focuses on a fixed repayment obligation rather than a potential increase in value.

While shares represent a stake in a company's equity and bonds are part of debt financing with a fixed repayment plan and interest, a loan is usually a more individual and flexible form of financing that is agreed between individuals or between individuals and financial institutions.

The legal basis for loan agreements in Germany is laid down in the German Civil Code (BGB), in particular in Sections 488 et seq. BGB.

Section 488 (1) sentence 1 BGB defines the nature of a loan agreement as follows: the lender is obliged to make the agreed amount of money available to the borrower, and the borrower undertakes in return to repay the amount received and to pay the agreed interest.

The elements of a loan agreement are complex, but they usually contain key points that include the following:

- Loan amount: The amount that is borrowed.

- Term: The period over which the loan is granted and by which it must be repaid.

- Interest rate: The percentage added to the loan amount and payable by the borrower as the cost of the loan.

- Repayment plan: A plan that specifies how the loan will be repaid, either in regular installments or as a lump sum at the end of the term.

- Collateral: Any collateral or guarantees intended to protect the lender in the event of default.

- Termination conditions: Conditions under which the contract can be terminated prematurely.

These components establish the legal basis for the obligations of both parties and define the framework for the financial relationship. A loan agreement must always protect the interests of both parties and be legally enforceable so that it can serve as a solid basis for financial transactions between the contracting parties.

By the way: With Beglaubigt.de, you can create a complete loan agreement tailored to your individual needs in just a few clicks.

The intuitive questionnaire allows you to customize the contract according to your preferences and ensure that all legal requirements are precisely met. (Click here for the loan agreement creator)

What is a loan agreement example?

Case study of a private loan agreement

Let's assume that Ms. Müller borrows €10,000 from her brother, Mr. Müller, in order to carry out urgent roof repairs on her house.

You agree that Ms. Müller will repay the money over a period of five years at an annual interest rate of 2%.

Repayment shall be made in annual installments of €2,040 each.

These terms and conditions are set out in writing in a loan agreement, which also stipulates that Ms. Müller grants her brother a mortgage on her house as collateral. The agreement also stipulates that no early repayment penalty will be charged in the event of early repayment of the loan in full.

Case study of a commercial loan agreement

Tech-Startup GmbH needs additional funds to finance a new product development and therefore takes out a loan of €200,000 from Bank X. The loan agreement provides for a term of ten years with a fixed interest rate of 4% per annum.

Repayment is to be made in monthly installments of around €2,027, which corresponds to an annuity repayment, whereby payments remain constant over the term and consist of an interest and principal component.

The bank has a mortgage on the company building as security. The contract also includes a clause that lets the company pay back the loan early, either fully or partly, at any time with three months' notice, but they'll have to pay an early repayment penalty.

Analysis and explanation of the sample contracts

In the private loan agreement between Ms. Müller and her brother, it is striking that the interest rates could be below the usual market level, which is not uncommon for loans between relatives.

Despite the family relationship, securing the loan with a mortgage demonstrates a formal need for security. In this case, the clause on early repayment penalties is designed to benefit the borrower.

The business loan taken out by Tech-Startup GmbH has typical elements of corporate financing, such as a higher interest rate, which reflects the greater risk for the bank.

Annuity repayment provides planning security for both parties. The option of early repayment offers the company flexibility, while the early repayment penalty compensates the bank for the potential loss of interest.

In both cases, the loan agreements reflect the financial conditions and risk appetite of the parties involved. They serve as legal documentation of the agreements and as security for the lender, as well as a commitment and repayment plan for the borrower.

Our tip: On the Beglaubigt.de platform, you can generate a customized loan agreement with just a few clicks of the mouse, which can be flexibly adapted to your personal requirements.

The user-friendly online service ensures that your contract can be individually configured while complying with all legal standards.

Click here for the tool: start.beglaubigt.de/darlehensvertrag

What does a loan agreement regulate?

A loan agreement is a document that sets out the specific terms and conditions of a loan agreement between a lender and a borrower. It creates a legal obligation to repay the borrowed money and specifies the circumstances and costs under which this should be done. Here are the main components of such an agreement and their significance:

1. Presentation of the contract contents and clauses:

- Parties to the agreement: Identification and addresses of the lender and borrower.

- Purpose of the contract: Clear statement of the purpose of the loan.

- Conclusion of contract: Place and date of conclusion of contract.

2. Loan amount and disbursement:

- Loan amount: The exact amount that is borrowed.

- Payment terms: Conditions under which the loan is made available, including the timing and method of payment.

3. Interest, term, and repayment:

- Interest rate: Determination of the interest rate applicable to the loan and how it is calculated (variable or fixed).

- Term: The time frame within which the loan must be repaid.

- Repayment schedule: Detailed list of repayment dates and amounts.

4. Collateral and warranties:

- Collateral: Description of any collateral, such as real estate, guarantees, or other assets.

- Guarantees: Any guarantees offered to the lender by the borrower or a third party.

5. Legal regulations and obligations of both parties:

- Obligations of the borrower: Repayment of the loan, interest payments, handling of collateral.

- Obligations of the lender: Provision of the loan amount, correct specification of interest rates, observance of notice periods.

6. Typical terms and conditions in loan agreements:

- Changes to the terms and conditions: Conditions under which contractual terms and conditions may be changed.

- Early repayment: Provisions governing the possibility of early repayment of the loan by the borrower.

- Default clauses: Conditions and consequences of late payments.

- Termination rights: Circumstances under which the contract can be terminated by either party.

7. Consequences of breach of contract:

- Delay: Measures and fees in the event of late payment.

- Breach of contract: Consequences of non-compliance with other contractual terms.

- Remedies: The steps that can be taken in the event of breaches of contract.

Each of these points is crucial for legal certainty and clarity in contractual relationships. It is common practice to set out these details in detail in order to avoid misunderstandings and ensure that both parties understand their rights and obligations.

The loan agreement serves as the legal basis for the loan relationship and must be available as a reference document in the event of disputes. (see: Private loan agreement template)

What is the difference between a loan and credit?

Definition and delimitation of terms:

- Loan (§ 488 BGB): A loan is a form of credit in which the borrower is provided with an agreed amount of money for a fixed term. The borrower undertakes to repay the amount at the end of the term and to pay interest. From a legal perspective, a loan is therefore a subtype of credit, as specified by the German Civil Code (BGB).

- Credit: The term "credit" is the generic term for any type of temporary provision of capital. It is generally broad in scope and includes not only loans but also other forms such as overdraft facilities, overdraft credit, supplier credit, and leasing. Credits can refer to both cash payments and payments in kind and are not necessarily tied to repayment in the same amount (e.g., in the case of interest on use).

Differences in contract design and execution:

- Loan agreement: A loan agreement is often subject to specific formal requirements and must meet certain legal requirements. The loan amount is usually paid out in a single sum, and repayment, including interest, is made according to a fixed schedule.

- Credit agreement: A credit agreement can be more flexible and may, for example, also include overdraft facilities on a checking account. The credit line can be used up to a certain maximum amount, and interest is only charged on the amount used.

Examples and practical implications of the differences:

- Loan example: A private individual takes out a mortgage loan to purchase a property. They receive the loan amount in a lump sum and repay it over the term of the loan with interest.

- Credit example: An entrepreneur uses an overdraft facility to ensure the liquidity of his company. The available credit line can be used flexibly, and interest is only charged on the amount actually used.

The practical implications of these differences are particularly evident in terms of flexibility and costs. While a loan is usually used for long-term financing with a fixed repayment plan, a credit facility offers more flexibility and can bridge short-term liquidity bottlenecks.

The costs for the borrower may be lower with a flexible loan agreement if the loan is not used in full or is only used for a short period of time. With a loan, on the other hand, the terms and interest rates are fixed for the entire term, which leads to greater planning security.